Extras din curs

UNIT 10

FINANCIAL STATEMENTS

READING SESSION

Read the following paragraphs:

The Balance Sheet

The Balance Sheet shows a company`s resources and financial position at a particular date and the provenance of these resources; it is prepared either at the end of the year or at the end of each month. The Balance Sheet contains a listing of items such as: assets, liabilities, owner `s equity. In a balance sheet cash is always the first asset listed. It portrays the overall financial position of the business at a specific date during these recurring cycles of investment, recovery of investment and reinvestment.

The Statement Of Cash Flow

Cash flows result from three major groups of activities :operating activities; investing activities; financing activities.

It is often prepared in order to give a full and complete picture of cash receipts and disbursements for an accounting period. It is useful in preparing a cash budget.

The Chart Of Accounts represents a list of accounts with their account numbers. It differs from one country to another for example in the U.K the chart of accounts consists of five classes while in France it has seven classes. The entries recorded on the left side of any account are called debits while entries recorded on the right side are called credits. The chart of account is conceived with the purpose of reflecting increases and decreases in monetary amounts resulting from business transactions.

U.K.

Class 1 – Assets

Class 2 – Liabilities

Class 3- Shareholders ` Equity/ Owner `s equity /Shareholders`/ stockholders `equity – in corporations/ Partners equity – in partnerships

Class 4 –Expenses

Class 5- Revenues

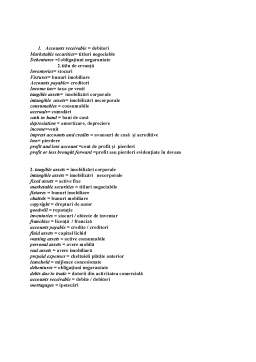

VOCABUARY:

Accounts receivable = debitori

Marketable securities= titluri negociable

Debentures =1obligaţiuni negarantate

2.titlu de creanţă

Inventories= stocuri

Fixtures= bunuri imobiliare

Accounts payable= creditori

Income tax= taxa pe venit

tangible assets= imobilizări corporale

intangible assets= imobilizări necorporale

consumables = consumabile

accruals= cumulări

cash in hand = bani de casă

depreciation = amortizare, depreciere

income=venit

imprest accounts and credits = avansuri de casă şi acreditive

loss= pierdere

profit and loss account =cont de profit şi pierderi

profit or loss brought forward =profit sau pierderi evidenţiate în devans

FOCUS ON LANGUAGE

Plans

Have you got anything fixed up for?

I was wondering if you had anything in mind for

Likes

I am in to

I am fond of

I am keen on

I enjoy / like / love

I do enjoy / do like / do love

There`s nothing I love / like more than

I`m crazy about

I take much interest in

Dislikes

I don`t like / love / enjoy

I dislike

I`m not crazy about

There`s nothing I love less than

I hate

I am not particularly keen on

CHECK YOUR UNDESTANDING

I. Translate into Romanian:

a. The Chart of Accounts

1. ASSETS 2. LIABILITIES

Current assets Current Liabilities

Cash Notes Payable

Cash in Checking Accounts Accounts Payable

Cash in Saving Accounts Salaries Payable

Cash on Hand Unearned Rent

Notes Receivable Revenue

Accounts Receivable

Inventory

Prepaid Rent

Prepaid Insurance

Supplies on Hand

Non-current Assets: Long Term Liabilities :

Equipment Mortgage Payable

Accumulated Depreciation: Equipment Bonds Payable

Buildings

Accumulated Depreciation: Buildings

Land

3. OWNER `S EQUITY

Capital

Withdrawals

4. REVENUE

Sales

Commission Earned

Rent Income

Interest Income

5. EXPENSES

Cost of Sales

Salaries Expense

Depreciation Expense

Rent Expense

Preview document

Conținut arhivă zip

- Finance Business English

- traduceri cuvinte.doc

- UNIT 10.doc

- UNIT 11.doc

- UNIT 12.doc

- unit13.doc

Alții au mai descărcat și

I. Utilizarea impozitului ca instrument Cea mai mare parte a resurselor publice sunt prelevari obligatorii si de aceea se impune definirea...

Propuneri privind cotele de impozit pe profit Nu se pot încheia aceste scurte consideratii asupra cotei de impunere, fara a fi exprimata opinia...

Infiintarea bancii nationale a romaniei (1880) Banca Nationala a Romaniei este prima institutie de emisiune a statului roman independent....

Resursele pietei eurodevizelor Resursele acestei piete au fost la origine plasamente facute de investitorii internationali sub forma depozitelor...

Te-ar putea interesa și

Introducere Mediul în care-şi desfăşoară activitatea instituţiile este tot mai complex şi imprevizibil, iar ritmurile schimbărilor acestuia este...

Capitolul I INTRODUCERE I.1. NECESITATEA ADAPTÃRII CONTINUTULUI CONTRACTELOR COMERCIALE INTERNATIONALE Încã de acum câteva decenii se vorbea...

INTRODUCTION This paper analyses the role of metaphors in business culture. As an abstract field of discourse, the world of business makes use of...

Introduction This project is an approach to the language of Business English as the title suggests it. I have presented here, the main aspects of...

Introducere Tranzacţiile internaţionale se dovedesc a fi printre cele mai complexe activităţi economice şi presupun atragerea unui volum...

1. Descrierea firmei SC Seytour SRL este a o agenție de turism tour operatoare, care fost înfiinţată în anul 1990 în România. În prezent, îşi...

Diferente intre AASB si FRC, AUASB, ASIC, APRA, ASX 13 Care sunt relatiile dintre AASB, Guvernul Australian si Organismele Profesiei Contabile...

Moneda Euro Moneda euro a apărut pentru prima dată în 1999, înlocuind așa-numita unitate monetară europeană (ECU) și fiind pusă în circulație la...