Extras din referat

Starting with 1948 (nationalization from 11 June) and until December 1989 (the moment of the fall of communism), the Romanian economy functioned according to the criteria specific to a centralized environment, being a planned (socialist) economy. Romanians applied a Soviet-style accounting imposed on Romania without too much talk, just like the economic system it was going to serve (Calu, Dumitru, Guse, Pitulice, Aurelia, & Eugeniu, 2011).

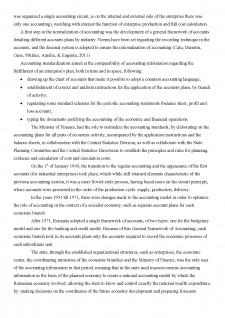

As mentioned and written by Krzywda, Bailey, & Schroeder (1995), the socialist doctrine means abandoning the mechanisms of market economy and replacing them with the specifics of the planned economy. They made the following comparison:

Elemental caracteristics

Market economy

Planned economy (socialist)

Means of production

Private property

Public (belong to the state)

Integration mechanism

Market

The plan

Enterprises

Autonomous

Dependent

Prices

Independent (real)

Controlled (artificial)

Banks

Commercial orientation

Focused on the plan

The role of accounting records

Accounting - Active role

Accounting - passive role

The reporting process

Outwardly oriented

Focused on domestic needs

Users

Enterprises and the state

Central Authorities

The institutionalization of the planned economy in close connection with the normalization required the reorganization of the accounting on the rationalization line and its normalization. The accounting culture in our country stood at that time under the sign of the ideology of the political system, the main purpose of standard accounting being to ensure documentation of the state plan, both in the elaboration phase and in the execution phase (Calu, Dumitru, Guse, Pitulice, Aurelia, & Eugeniu, 2011).

The goals to be achieved by accounting during the socialist era were:

- centralized control and planning of the economy;

- evaluating and tracking the performance of the enterprise by directly reporting the planned costs and costs;

- the privileged information of state bodies, the dominant and unique user of accounting information.

As mentioned in Calu, Dumitru, Guse, Pitulice, Aurelia, & Eugeniu (2011), accounting was considered a tool for controlling the execution of the plan and a means of defending the integrity of state property. The accounting was organized in one informational circuit (monism accounting - at the level of the enterprise

was organized a single accounting circuit, ie on the internal and external side of the enterprise there was only one accounting), watching with interest the function of enterprise production and full cost calculation.

A first step in the normalization of accounting was the development of a general framework of accounts detailing different accounts plans by industry. Norms have been set regarding the recording technique in the accounts, and the decimal system is adopted to ensure the rationalization of accounting (Calu, Dumitru, Guse, Pitulice, Aurelia, & Eugeniu, 2011).

Preview document

Conținut arhivă zip

- Accounting Model in Communist Romania, year 1949 - 1989.pdf