Extras din seminar

THE ACCOUNT

The account is the basic unit used in accounting to summarise business transactions. Accounts are classified as follows:

Øassets

Øliabilities

Øowner’s equity

Assets are economic resources owned or controlled by an entity as a result of past transactions, which are expected to be of benefit in the future. Exemples of assets are:

- cash (refers to coin, currency, cheques etc.)

- accounts receivable. When a business sells goods or services on credit, the

Accounts Receivable account records these transactions.

- land

- office equipment

- office furniture.

A separate account is kept for each type of asset.

Liabilities represents economic entity’s future obligation as a result of past transactions.

Examples of liabilities are:

- accounts payable. When a business purchases goods or services on credit,

the Accounts Payable accuont records these transactions. It is the opposite

of the Accounts Receivable account.

- mortgage

A separate account is kept for each type of liability.

Owner’s Equity is the owner’s claim on the assets of the business. Owner’s equity is increased with revenue and decreased by expenses or an owner’s withdrawal.

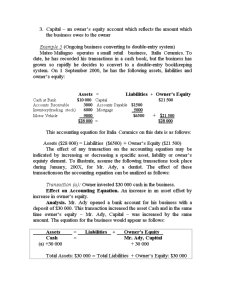

ACCOUNTING EQUATION

The relationship between the three basic accounting elements – assets, liabilities and owner’s equity – is expressed in the accounting equation, shown as follows:

Assets = Equities

Creditors Owner

Assets = Liabilities + Owner’s Equity

The equation shows assets are equal to equities. Equities are divided into liabilities and owner’s equity. When the amounts of any two of these elements (assets, liabilities or owner’s equity) are known, the third can be calculated, as follows:

Assets = Liabilities + Owners Equity

or

Owner’s Equity = Assets - Liabilities

or

Liabilities = Assets – Owner’s Equity

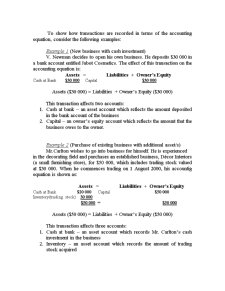

TRANSACTIONS AND THE ACCOUNTING EQUATION

In accountig terms, a transaction is defined as an event which affects the financial position of a business. It involves the exchange of money for money’s worth of goods or services between two parties. Buying and selling goods and receiving or paying money are transactions. There are two main types of transaction:

- cash – where money is received in exchange for goods or services

- credit – where goods or services are supplied or received on

agreement that payment will be made at a later date.

The transaction is the basic operating unit of the business. Cash is

used to purchase goods, these goods are then sold, and the cash received for them is used to purchase more goods which, in turn, are sold. This cycle of cash à goods à cash is called the operating cycle. Below is a simple illustration of the operating cycle for both cash and credit transactions.

Preview document

Conținut arhivă zip

- Accounting Practice.doc

Alții au mai descărcat și

1.1.CONTABILITATEA SI IMAGINEA FIDELA ASUPRA ENTITATII Una din princip.functii ale contab era inregistrarea tranzactiilor cu furnizprii si...

Societatea A prezintă la 31.12.N următoarele informaţii, preluate din balanţa de verificare finală (u.m.): 1. Cheltuieli de constituire 5.000 2....

- Întreprinderea – agent economic principal Există 4 categorii principale de agenţi economici: - Întreprinderea – agent economic principal care...

3. Organizarea si functionarea IC 3.1 Cadrul juridic de organizare si functionare a IC IC sunt organizatii in conformitate cu prevederile legii...

Exemplul 1 În vederea constituirii S.C. „DIO” S.R.L. conform contractului şi statutului societăţii se subscrie un capital social de 20.000.000 lei...

A. Riscul şi rentabilitatea unei acţiuni Problema 1. La momentul t = 0 preţul acţiunii A este P 1000 0 = u.m. La momentul t = 1, preţul acţiunii...

Aplicatie O societate comerciala are cont deschis la BCR-SMB la 1.04. Se detine in cont 150.000. In cursul lunii aprilie, banca efectueaza...

In cadrul acestor activitati, problema principala se refera la determinarea si gestionarea costurilor de productie. Determinarea costului unitary...

Te-ar putea interesa și

Varietatea si complexitatea aspectelor legate de buna gestionare a trezoreriei întreprinderii creeaza un amplu câmp de analiza si dezbatere pentru...

În literatura de specialitate, guvernanța corporativă cuprinde ansamblul de reguli și principii după care funcționează o întreprindere, modul de...

Introduction Economics is part of our life, either we are students at the Faculty of Languages, a banker or a simple tax payer, we all deal with...

Introducere Spre deosebire de multe alte profesii moderne, contabilitatea are o istorie care este, de obicei, discutată în termenii unui eveniment...

Situaţiile finaciare trebuie să prezinte fidel poziţia financiară, performanţa financiară şi fluxurile de numerar ale unei întreprinderi. Aplicarea...

1. SISTEMUL CONTABIL DIN JAPONIA 1.1. Contextul contabil Industrializarea Japoniei a început în anul 1868 după restauraţia Meiji. Guvernul era...

1. Introducere Conceptul de trezorerie apare ca rezultat al unei lungi evoluţii istorice, care a condus mai intâi, la identificarea noţiunii de...

INTRODUCERE: Contabilitatea isi incepe istoria in Evul Mediu, fiind o necesitate la dezvoltarea economiei monetare si aparitia germenilor...